With those words, Mason Shoe Chairman Bill Scobie wraps up his pitch for potential customers of his company to sign up for Mason Direct Credit, which in the case of the person whose catalog arrived at my home allows for a credit line of $500 to buy shoes, boots, slippers and/or a few accessories.

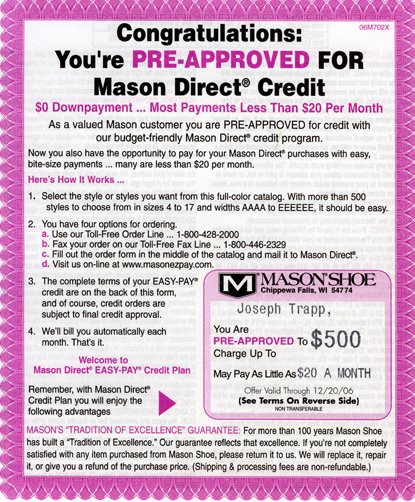

The catalog has two front-page refers to the program, in addition to the open letter from Scobie on Page 2, a Web address at the bottom of every page and a pull-out sheet headed "Congratulations: You're PRE-APPROVED FOR Mason Direct Credit" that give some details of the program.

The pull-out sheet is in magenta and black and has a frilly border of the sort you saw on the Elks Club Hoop Shoot certificate you got after a middle-school free-throw contest.

I didn't see any hint of finance charges. Flipping through the catalog, I saw that all the shoes have little inset breakdowns of the price per month, but the fine print on each page says "the price per month reflects merchandise price only. Actual monthly payment may vary..."

Although No. 3 on the certificate pictured here says that all the terms are on the "back" of the form, when you flip it over you find only some terms, including overdraft and late charges, how payments need to be made, a definition of default, some other provisions and a paragraph on arbitration.

What gives? Where's the rest of the fine print?

Well, at the back of the catalog is the other half of the pull-out sheet (of which there was no mention at the front of the catalog), which - Surprise! - outlines the annual percentage rates and "privacy" policy.

The APR is predictably high (though not in Arkansas, where it is listed at 6 percent) and the "privacy" policy is a joke. Unless you opt out, Mason Shoe may share your "nonpublic personal information" with pretty much anybody they like.

Now, I'm not saying they're painting a target on people of limited means, but they are trying to attract people who need to pay for a pair of shoes in installments...

1 comment:

Yeah, and those are for shoes that retail for 40 bucks. Totally puts things in perspective. It's hard to remember that even as our cars are "junkers" and we grapple with whether we have enough dough to buy a new one, in comparison to those who have to buy shoes on an installment plan of 15 bucks a month, we really are among the privileged class. Instead of depressive realism, you got a healthy dose of whatever the opposite of relative deprivation is. So much better than coming home to a credit card bill :-)

Post a Comment